The Nepali rupee (NPR) has been pegged to the Indian rupee (INR) for a long time. The current fixed pegging of 100 INR to 160 NPR was established in 1993 and has been in practice for over thirty years now. The fixed exchange rate of 1.6 was determined based on the macroeconomic and historical factors of the two countries that were relevant at the time of peg establishment.

Many of those decision factors have now either changed or do not exist; however, the fixed pegging scheme continues to be in circulation the same way as it has been since the beginning. Surprisingly, Nepal appears to be in ‘no rush’ to reform the pegging policy, at least, for the foreseeable future.

In this context, it is important to note that while the pegging mechanism is fixed; it still requires active control of the NPR/INR rate through foreign exchange interventions. In the process, Nepal Rastra Bank (NRB) decides on a buy-sell spread around the official 1.6 rates based on the current market conditions.

For instance, when the market exchange rate exceeds 1.6 NPR per INR, NRB purchases US dollars to appreciate the rupee back to the official peg. This strategy, also called a Band-Aid model (keeping exchange rates within a predetermined range), involves regulating excess rupee liquidity and preventing significant deviations from the 1.6 rate threshold. This arrangement has impacted Nepal’s economy by affecting trade, monetary policy, and overall business commercial stability. This article argues that a much-needed reform related to the fixed pegging policy cannot wait too long based on the current and emerging economic realities.

Why do we need to reform the fixed pegging?

The fixed pegging was required back then to address the currency crisis related to Nepal’s balance of payments. The proponents of the fixed pegging claim that the fixed exchange rate helped mitigate uncertainties in business transactions, provided confidence and predictability in the Nepali currency market and helped bring stability to Nepal’s trade partnership with India.

While these arguments are largely held in times of economic and political instability in the country, the other side of the story is utterly overlooked by the policymakers. There are convincing hard facts and evidence to support the case that the time has finally arrived for monetary policy reform grounded on the last three decades of fixed-pegging experience.

First and foremost, given the size of the economy, Nepal does not have any influence on India’s monetary policies; however, it is essentially compelled to adopt them. Nepal’s actions are dictated by the decisions made by the Reserve Bank of India (RBI) whenever it decides to raise or lower interest rates. Likewise, when the Indian rupee’s value strengthens or weakens against key global currencies, Nepal’s currency is also affected. This fixed pegging approach essentially brings in inflation and monetary fluctuations from India into Nepal and increases the volatility of prices in the Nepali markets.

Second, the fixed pegging arrangement promotes an informal flow of funds between the two countries. This can potentially result in loss of taxable revenue from transactions made in the informal economy. Nepal imposes certain capital restrictions and maintains relatively restrained interest rates compared to India. This dynamic encourages Indian funds to be informally moved into Nepal to exploit the interest rate differences causing further worsening of the trade deficits due to under-reported or hidden transactions.

Third, the unwavering 1.6 exchange rate has caused a considerable overvaluation of NPR against currencies other than the INR. The impact of this situation has affected Nepal’s ability to compete in international trade. The consequences were evident from the relentless geometric growth of total trade deficits in the past decades, in which a substantial portion of the deficits is directly or indirectly tied to the fixed pegging.

Fourth, Nepal’s current account and balance of payments have deteriorated over time. As time goes by, the fixed pegging approach further intensifies its economic dependence on India, making it vulnerable to supply shortages and market distortions.

For example, in the recent Covid pandemic, border closures led to shortages of essential goods within Nepal. Similarly, the hardships during the multiple unofficial economic blockades in the past few decades are still fresh in Nepalese memory. In those situations, NRB must be proactive in building up necessary currency reserves as a protective measure to escape the cycle of deep dependence on India.

Fifth, the NRB’s frequent actions in defence of the peg causes a rapid depletion of the nation’s foreign exchange reserves. For example, foreign reserves shrank from USD 9.5 billion to USD 9.1 billion between July 2021 and May 2022 due to NRB’s selling of dollars in the market (Nepal Rastra Bank, 2022). This unsustainable exhaustion of foreign currency has hindered Nepal’s domestic financial markets, institutions, and capital account activities. Thus, in essence, Nepal has practically outsourced its monetary and exchange rate policies to India.

Additionally, there has been a notable change in economic relations between India and Nepal in recent times. In 1993, the introduction of the peg happened when India had a significant influence on Nepal’s commerce, trade, and economy. However, since then, Nepal has made a conscious effort to expand and diversify its trade opportunities by establishing relationships with various countries such as China, Bangladesh, the United Arab Emirates, the European Union, and the United States. This has resulted in the trade patterns with India going down at a modest pace. As of 2021, the percentage of trade between Nepal and India stands at about 60 per cent.

Furthermore, while Nepal’s economy still relies heavily on agriculture and remittances. Nepal is seeing an increase in foreign direct investment from countries other than India, particularly in sectors like infrastructure, hydroelectricity, and tourism.

In contrast, India is undergoing rapid expansion of service industries and heightened private spending. India is attracting multinational companies and heavily investing in software technologies. These differing structural trajectories of the two economies make the original rationale of Nepal adopting India’s monetary policy less compelling.

Therefore, the need for Nepal to establish monetary policies tailored to its unique economic framework has become more pressing than ever. Now is indeed a critical moment for Nepal to deeply consider the monetary policy reforms concerning the fixed currency peg.

The path forward

A gradual and calibrated approach is necessary for a transition strategy. This requires a thorough assessment, research, and strategic planning before making a significant adjustment. Over the past three decades of fixed pegging, Nepal’s policy-making institutions such as NRB should have learned from what has worked and what has not. By implementing effective macroeconomic management and applying these lessons learned, Nepal can secure ongoing trade and remittance flows without being tethered to a fixed peg.

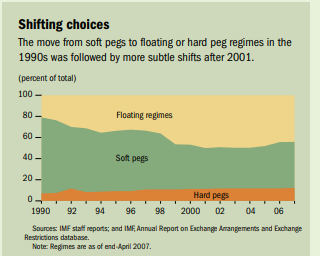

More importantly, there are viable alternatives available. For example, implementing a managed floating exchange rate regime that involves fixing the exchange rate in relation to a combination of four major global currencies – the Indian rupee, Chinese Yuan, US Dollar, and Euro. This mix could be tailored to Nepal’s major trading partners. In this scenario, NRB would play an active role in managing the exchange rate, preserving stability while introducing a degree of adaptability. According to the IMF, the floating regimes are actually gaining more traction in recent years.

Another best option could be to follow the model adopted by many other countries in the world such as Saudi Arabia, UAE, Panama, etc., in which local currencies are pegged with the US dollar, which is perhaps the most stable and secured currency in the world.

Nevertheless, the question of the peg should align with the broader discussions on Nepal’s development model. NRB’s research department and think tanks should conduct extensive technical studies comparing the peg regime’s efficacy to alternative strategies proposed. The decision should be driven based on economic hard facts rather than on geo-political factors. Extensive debates involving all stakeholders can then find the way forward for a truly sovereign monetary system. Thus, while the INR peg has fulfilled its purpose for more than 30 years, its limitations are now evident and cannot be simply ignored. The necessary monetary reform in this regard is imminent.