Digital payments have entered into everyday life on all sides of the world. For Nepal, a country that is fast making strides to catch up with technology, the birth of Unified Payment Interface (UPI) has opened newer avenues. UPI in Nepal started in March 2024, with active works to make the money transfers simple, inclusive, faster, and easier for all.

UPI-Nepal’s story of collaboration for the digital payment revolution will highlight the major plus points, mostly emerging concerns, and the possible outlook for businesses and individuals. So, there needs an understanding about how UPI integration is expanding the realm of digital payments in Nepal in 2025, including its benefits, challenges, and how it helps merchants and eases cross-border transactions to shape the future of fintech in Nepal.

What is UPI and why is it important for Nepal?

UPI, developed by India’s National Payments Corporation of India (NPCI), facilitates real-time payment. Money can be directly transferred from one bank account to another without fixing account numbers or IFSC Codes, using a Virtual Payment Address (VPA).

In India, this payment platform has created a whole different payment ecosystem. And now, Nepal has become a full-fledged adopter of UPI for cross-border payments through cooperation between Nepal Rastra Bank (NRB) and NPCI International Payments Limited (NIPL).

According to NRB reports, by June 2024, over 100,000 UPI transactions worth Rs 250 million have been made in Nepal, which is a good indicator of fast adoption.

Why UPI is a game-changer in Nepal?

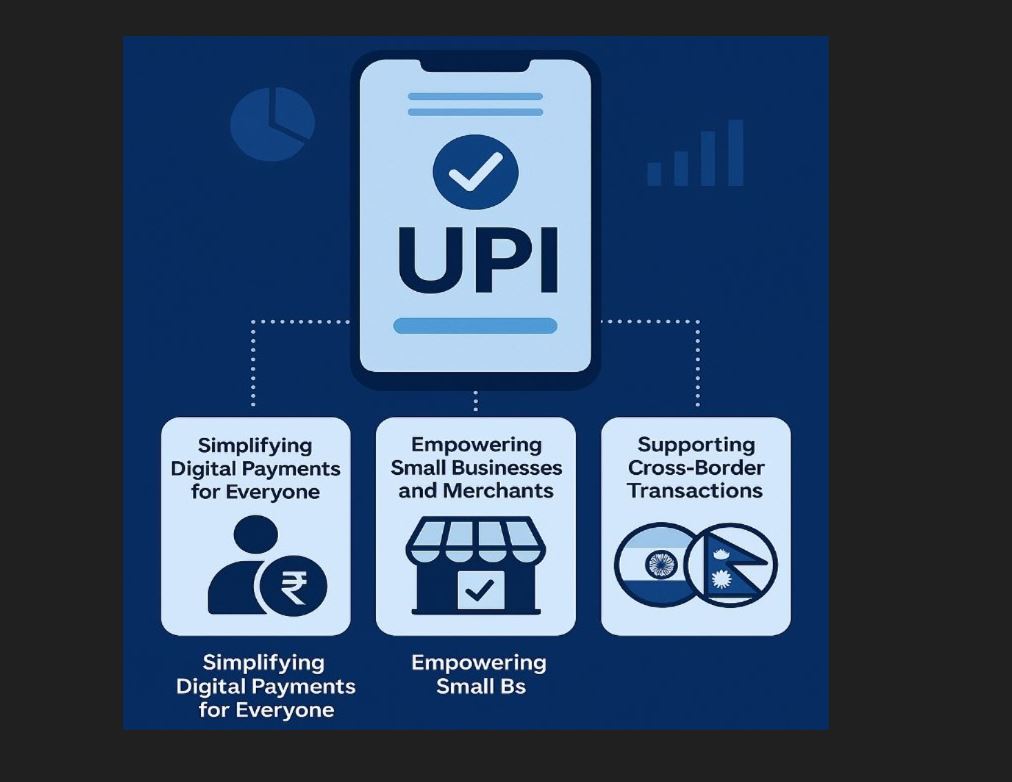

UPI is a game-changer in Nepal. The reasons are explained below:

1. Basic digital payments for everyone: Users in Nepal had to rely on separate individual wallets like eSewa or Khalti by IME, each with very little interoperability. Transferring money from users who were using different platforms was not easy. With UPI, all that is unnecessary; only a VPA, which is like an email ID, is required to send or receive dollars instantly irrespective of the bank and/or wallet.

2. Promoting empowerment for local businessmen and merchants: The payments via UPI enable small shopkeepers, street vendors, and local entrepreneurs to accept money by QR codes and without costly hardware payments one has to encounter while transacting through a POS machine. Example: A momo stall owner in Kathmandu or a tea vendor in Birgunj can now accept payments using any UPI-linked app, thus, lowering dependence on cash and enticing digital-savvy customers.

So the benefits users get is low cost with minimal to zero transaction fees. It is also convenient where payments can be received instantly with QR codes. At the end it is secure where transactions are verified and traceable.

3. Strengthening cross-border transactions between Nepal and India: Millions of Nepali trickle in and work in India, while many of them often have to remit back into Nepal. Genuine methods of remittance is usually slow, costly, and tedious. The UPI integration between Nepal and India makes cross-border payments: instant, cheap and transparent. Thus, the UPI system links people from both countries, giving split-course between informal and cash remittance systems.

What are the challenges to UPI integration in Nepal?

Notwithstanding its promise, there are a few practical obstacles to UPI integration in Nepal. Firstly, most of the rural areas continue to face connectivity issues, and older generations may be reluctant on using digital apps.

Secondly, it’s important to keep India and Nepal working together, manage exchange rates, and follow the law. Following and implementing uniform pegged exchange rate practices in both countries sometimes seem to be a hard thing to implement due to different social, economical and political issues.

Then, many people are still deterred by the fear of fraud and digital mistakes which shows lack of trust and awareness. It is imperative to enact strong consumer protection legislation and launch awareness-raising initiatives.

What happens next?

Nepal Rastra Bank has ambitious goals. It is expected that the following systems will be integrated with UPI: fintech innovation (microloans, digital insurance, and investment apps) and government payment systems (social security, pensions).

There is a lot of potential, but telecom companies, banks, regulators, and fintech companies need to work together. In short, a financial revolution is happening in Nepal.

UPI is a digital finance revolution, not just a new way to pay. It makes Nepal hopeful in bringing a revolution on how small businesses are growing and payments are done these days, further lowering down remittance costs, and providing more access of financial services to all class of business communities, individuals and household.

UPI is a faster, safer, and clear way for students, shopkeepers, and migrant workers to handle their money. But for it to work, people need to know about it, trust it, and have the right support.